04/18/2015 - Financial Repression Explained: It’s about Macro Prudential Policies to Control and Reduce Government Debt

WSJ article highlights how as interest rate benchmarks go negative, banks may be paying borrowers .. “Negative interest rates in Europe have created a previously inconceivable problem for some banks: They may soon have to pay interest to customers who borrow from them .. The novel problem is just one of many challenges caused by negative interest rates. All over Europe, banks are being forced to rebuild computer programs, update legal documents and redo spreadsheets to account for negative rates . Banks, hoping to avoid the expense of having to pay their borrowers, are turning to central banks for guidance. But what they are hearing is less than comforting.” .. it’s financial repression.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

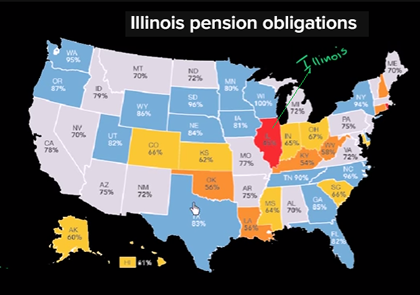

04/18/2015 - MISH SHEDLOCK talks AMERICA’S PENSION PROBLEM

Mish Shedlock talks about the magnitude of the mounting Pension Problem in America and uses his home state of Illinois as a prime example. According to a State Budget Solutions, last year’s state unfunded pensions reached an all-time high of $4.7 trillion. This funding gap state public pension plans are underfunded by $4.7 trillion, up from $4.1 trillion in 2013. Overall, the combined plans’ funded status has dipped three percentage points to 36%. Split among all Americans, the unfunded liability is over $15,000 per person.

ILLINOIS’ PENDING PENSION CRISIS

“Illinois Pension’s in general are 39% funded! This is after this massive rally we have had since 2009 in financial assets. Some of the worst ones are only about 20% funded. I think the Teacher’s Pension Plan is about that and the General Assembly and Judicial Pension Plan are also on the bottom.”

“Various cities in Illinois have problems, Chicago being one of them. The City of Chicago has a huge pension crisis right now. We have things in Illinois like “Home Rule Taxes” where cities can levy their own taxes in addition to the state. That is why we have varying sales tax that range anywhere from 6% to 10%, depending on locality.”

“I believe Chicago is Bankrupt!”

“I have been working with the Illinois Policy Institute. There are a number of cities in Illinois (I am not going to name them), but I am aware of five cities (one of them a major city – not Chicago) that are ready to file bankruptsy – and it is all over the pension issue! The problem is they can’t file bankruptcy because the state doesn’t allow it.”

“The fundamental problem is they have made more promises than they can possibly keep!”

GAMING THE PENSION SYSTEM

The problem is “you have police and fire workers who can retire after 20 years … and collect up to 70% of their earnings based on the 5 highest years salaries. We see a lot of pension spiking in the last few years where for example police work overtime (which counts towards their best five years) so these workers stand to collect far more in retirement (total years in retirement) than they actually ever made while working (total years worked).

“Tax payers are actually funding the employees portion of the pensions by excessive wages and direct contributions “.

“Chicago (has) floated General Obligation Bonds to actually just fund current expenses. That is illegal! We have bonds here in Illinois that are called tax exempt on the basis they are supposed to be funding long term infrastructure expenses that are funding short term needs.”

PROPERTY TAXES THE JURISDICTION OF UNDERFUNDED CITIES & TOWNS

“Taxes in Illinois are are already obscene. A homeowner on a $600,000 home can expect to pay $14-15,000 per year – every year on property taxes. Do you really own your own home in Illinois? On top of tht you have 10% sales tax.”

“Pensions are so underfunded in Illinois that they are going to go bust in the next slowdown. I believe one (a slowdown) is on the way.”

THE NEW, LOOMING PROBLEM FOR STATES, CITIES AND TOWNS

Negative interest rates are sweeping the globe. How will states, cities and towns fund themselves and their pension obligations in an era of potential negative nominal bond rates?

Returns on the heavily weighted funds’ bond holdings are being potentially destroyed , while

State bond offerings are likely to face mounting issues around maintaining investor attraction with such monstrous overhang levels of unfunded pension liabilities.

“How will states, cities and towns fund (attract) long term assets with 15 year negative bonds?”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/17/2015 - Financial Repression is Making Economies Less Dynamic

American Thinker posted essay emphasizes the negative, long-term effects of massive money printing through quantitative easing (QE) & of the zero interest rate policy (ZIRP) .. it’s all about the financial repression of interest rates – the thinking being that if this were not done, the pain of allowing the free markets to determine interest rates would be unbearable – “One need only imagine the bipartisan political panic were the interest paid by the U.S. federal government on its debt to double or triple, squeezing out hundreds of billions of dollars of spending on military and social programs. It is becoming ever more obvious to ever more people that sustaining these ‘financial repression’ policies is making economies ever more comatose; ever less dynamic. Exactly when the accumulating long-term economic damage becomes more onerous to central bankers and politicians than the short-term damage of ending QE and ZIRP can’t be known. But that inflection point will come, desired or not; willed or not. It is not avoidable.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/16/2015 - Financial Repression is a Weapon of Mass Financial Destruction

“Central bank financial repression results in the systematic and severe mispricing of financial assets. And that has sweeping consequences far beyond the windfalls it bestows on the thin slice of mankind that frequents the casinos of Wall Street, London, Tokyo and Shanghai. The fact is, the prices of money, debt, equity, traded commodities and all their derivatives comprise a vast and instantaneous signaling system that cascades through every nook and cranny of the real economy.Since the Greenspan age of financial repression in the late 1980s, the returns to savings have been obliterated while the rewards for speculation have soared. That’s important because only savings from production & income generate primary capital that can foster future wealth. Leveraged speculation merely causes existing assets to be re-priced & a temporary redistribution of paper wealth from the cautious to the exuberant. .. Financial repression is a weapon of mass financial destruction.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/11/2015 - FINANCIAL REPRESSION IN INDIA

Savings are important for an economy to be able to invest and grow at a healthy pace. Household sector is an important contributor to savings in an economy. However, in India, savings in the household sector has declined significantly in recent years and has come down from the level of 25.2% of the gross domestic product (GDP) in 2009-10 to 17.8% of the GDP in 2013-14. Financial savings in the household sector also declined from 12% of GDP to 7.2% during the same period. Although savings in physical assets went up from the level of 13.4% of GDP in 2004-05 to 15.8% in 2011-12, it also declined thereafter along with overall savings rate. The decline in financial savings is a matter of concern for policymakers as it can affect growth potential. One of the biggest reasons for the decline in savings rate, and in financial savings in particular, is attributed to financial repression.

SLR (STATUTORY LIQUIDITY RATIO) REQUIREMENTS

In India SLR requirements mandate banks to hold certain types of assets, such as government bonds, which suppress the real interest rate in the marketplace.

“The SLR is a form of financial repression where the government pre-empts domestic savings at the expense of the private sector. Real interest rates are lower than they would be otherwise,” said the Economic Survey.

Through SLR requirements, banks are used as captive investors in government bonds, which allows the government to finance its fiscal deficit at a relatively lower cost. The Reserve Bank of India in recent times has gradually reduced the SLR requirement for banks from 25% to 21.5% of demand and time liability. While it will take some time for the central bank to bring down this requirement, which will lead to better discovery of interest rates, the current higher real interest rates due to lower inflation is widely expected to boost financial savings.

Simply put, financial repression means that savers are not adequately compensated for their savings. “The Indian banking system is afflicted by what might be called ‘double financial repression’.

Financial Repression on the Asset side of the balance sheet

Financial repression on the asset side of the balance sheet is created by the statutory liquidity ratio (SLR) requirement that forces banks to hold government securities, and priority sector lending that forces resource deployment in less-than-fully efficient ways.

Financial Repression on the Liability side

Financial repression on the liability side has arisen from high inflation since 2007, leading to negative real interest rates, and a sharp reduction in households’ financial savings,” noted the Economic Survey 2014-15.

In a 2012 National Bureau of Economic Research paper, Debt Overhangs: Past and Present, Carmen M. Reinhart, Vincent R. Reinhart and Kenneth S. Rogoff noted:

“Financial repression includes directed lending to the government by captive domestic audiences (such as pension funds or domestic banks), explicit or implicit caps on interest rates, regulation of cross-border capital movements, and a tighter connection between government and banks, either explicitly through public ownership of some of the banks or through heavy ‘moral suasion’.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/10/2015 - Capital Controls in the form of “PFIC” Passive Foreign Investment Company

International Man’s Nick Giambruno explains the difficulty for Americans abroad to invest in non-U.S. based investments .. in this case it is called Passive Foreign Investment Company (PFIC) – the could be “foreign” mutual funds or “foreign” stocks

“the complexity of the paperwork for Americans to file when investing in PFIC makes it so onerous & legally prone to risk that it is effectively just not worth it & outright dangerous for Americans to do so – as such, the U.S. is effectively “forcing” Americans to keep their money at home & invested in U.S.-based investments”

Taking a step back and looking at the big picture, it’s clear the PFIC rules are part of the long-term trend of the U.S. government using burdensome regulations to effectively shrink the number of options available for those seeking to diversify internationally. These roadblocks are a clue as to how desperate and bankrupt it really is.

You shouldn’t be deterred, as that is exactly what the politicians want to happen. They prefer your savings remain within their immediate reach so that it’s easier to fleece.”

“Capital controls are used by many countries and come in all sorts of shapes, sizes, and labels. The purpose, however, is always the same: to restrict and control the free flow of money into and out of a country so that the politicians have more wealth at their disposal to plunder.“

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/10/2015 - “A Time of Unprecedented Financial Repression”

“We live in a time of unprecedented financial repression. As I have continued writing about this, I have become increasingly angry about the fact that central banks almost everywhere have decided to address the economic woes of the world by driving down the returns on the savings of those who can least afford it – retirees and pensioners.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

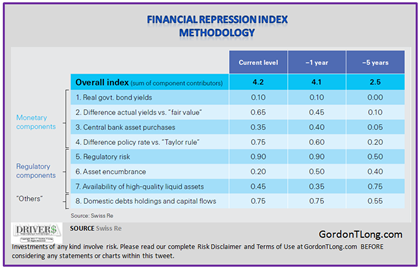

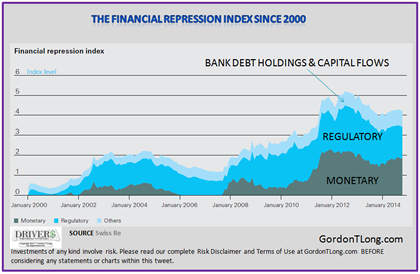

04/09/2015 - Financial Repression Index

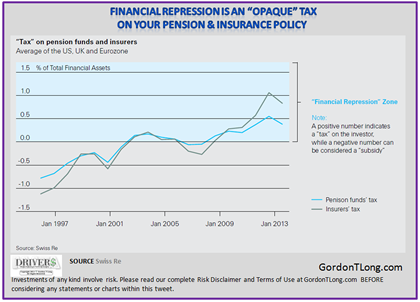

Swiss Re’s FINANCIAL REPRESSION INDEX demonstrates that mainline investment institutions are beginning to see what the FINANCIAL REPRESSION AUTHORITY has been shouting for some time!

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/09/2015 - Financial Repression Wealth Confiscation: Bailin Ahead for Greece?

“The loans to Greece by the ECB have been increasing, so the ECB has been increasing its credit exposure to that country. Second, the deposit runs that are occurring in the Greek banks have been accelerating over the past three months and they continue as we speak. So you have these two lines converging. The ECB is never going to allow those two lines to cross because if they did the ECB’s credit exposure would be larger than the amount of deposits in the Greek banking system. And if that were to occur, the ECB would never be able to get its loans to Greece repaid. When Cyprus failed, they (Western central planners) said that bank bail-ins were going to be the blueprint for other countries. And we have to look at what happened in Cyprus and apply it to Greece. When those two lines were converging in Cyprus, the ECB, IMF and the EU basically took over and nationalized two of the Cypriot banks — took the deposits out of those Cypriot banks and used those deposits to repay the ECB loans to Cyprus. So the same thing is going to be happening to Greece. The ECB is going to take the deposits out of the Greek banks and use those to repay all of the loans that the ECB has made to Greece. …. I think we should be worrying about whether this is going to be happening over this weekend.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/06/2015 - Leo Kolivakis: Pension Pulse Talks Pension Poverty

Special Guest: Leo Kolivakis – Pension Analyst & Publisher, PensionPulse.blogspot.com

Leo Kolivakis brings a unique perspective to Pensions having worked on both the Buy & Sell side as a Pension Plan analyst.

TITANIC GLOBAL BATTLE

Kolivakis sees a titanic battle going on around the world between Inflation & Deflation with the world shifting due to demographics, private / public debt problems and a global jobs crisis. As a result he sees bond yields falling because it is resulting in no inflation. “The bond market is rightly concerned about tight fiscal policy and austerity in a world of low growth, low inflation (possibly deflation) for a prolonged period of time”. “I am more worried about what is going on in China .. if you have a boom-bust scenario in China, the potential to import deflation (ie through lower goods prices, currency devaluation etc) is a significant concern”.

PENSIONS IN PERIL

“I believe there is a Private and Public Pension Crisis in America that needs to be openly discussed by US citizens & politicians. The private savings crisis in America shows the median 401K balance is under $20,000 and somewhere around $76,000 for people 60-65 years of age. That is definitely not enough money to retire comfortably for the rest of your life!”

“In the private sector where corporations are cutting defined benefit programs and going to low cost defined contribution plans, there is another crisis happening.” People are being forced to take on the responsibility of pension investment management decisions.

“Individuals are now caring the risk of their retirement!”

“What people don’t realize is the shift to Defined Contributions is very deflationary. People simply don’t spend as much as they do on Defined Benefits when they have known fixed incomes.”

PENSION POVERTY

DEFINED BENEFITS – A massive underfunding problem between $7 – $10T

CONTRIBUTORY BENEFITS – Median 401K Levels of $18,400 are ‘orders of magnitude’ short,

SELF FUNDING – IRA and Roth Plans are not earning the levels of income required for retirement. Market draw-downs have seriously impaired long term growth,

SAVINGS RATES – Falling Real Disposable Income is increasingly limiting already extremely low personal savings rates.

GOVERNANCE PROBLEMS

“There is a huge problem with the Public Pension Funds in the United States. The problem focuses around the governance model. It is all wrong! They have way too much political interference. They don’t have proper pension fund plan managers that can take internal actions, lower the costs of the funds and … match assets with liabilities”

“The US needs to consider privatizing Social Security and creating independent investment boards.”

“What is going on in the US right now is you have a lot of investment consulting shops that are typically forcing these public pension funds to invest in very high fee, high risk private equity / hedge funds. That is fine for the Private Equity Funds and Hedge Funds but it is not in the best interest of these public pension funds. I don’t think it is. As a matter of fact I know it is not!”

“The US really needs to reform its Public Pension Plans. To introduce shared risk models so that the risk of the plan is shared between the stakeholders (i.e. the employees), the government and the pension. They need to reform the governance so they start to pay the pension plan managers properly to manage more and more of the assets internally”.

“Pension Investments Are Fueling Inequality! The migration of Pension Plans to Alternative Investments such as Private Equity / Hedge Funds are contributing to the growth in Inequality”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/04/2015 - How Can and How Do Governments Address Their Debt Burdens? Paper by Carmen Reinhart & M. Belen Sbrancia

Article which summarizes the thoughts from Carmen Reinhart & M. Belen Sbrancia .. abstract from their original 2011 Paper: “Historically, periods of high indebtedness have been associated with a rising incidence of default or restructuring of public and private debts. A subtle type of debt restructuring takes the form of ‘financial repression.’ Financial repression includes directed lending to government by captive domestic audiences (such as pension funds), explicit or implicit caps on interest rates, regulation of cross-border capital movements, and (generally) a tighter connection between government and banks…Inflation need not take market participants entirely by surprise and, in effect, it need not be very high (by historic standards)…We describe some of the regulatory measures and policy actions that characterized the heyday of the financial repression era.”.. This article emphasizes how actual events in the current marketplace suggest the U.S. & other high debt/GDP countries are using history as a guide to help them liquidate debt in a politically feasible manner .. Here are some simple examples of possible financial repression in the marketplace:

1. Heavy handed regulation & control of financial institutions is well underway (first step in facilitating financial repression). All of this regulation is being marketed as “for the public good.”

2. Governments are playing a larger & larger role in government bond markets .. It is no longer possible to look at a yield curve & believe it reflects market-priced risk.

3. Governments are pushing for more & more domestic debt ownership.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/04/2015 - The Hidden Dangers of Financial Repression

Chris Whalen* explains the dangers of keeping interest rates too low for too long .. zero interest rates & quantitative easing, or QE, are actually making deflation worse .. “These policies are also causing a precipitous decline in consumer demand, which is visible in lower prices for key commodities such as copper, oil and natural gas. And they come at a long-term cost to individual investors and financial institutions .. Zero rate policy as practiced by the Fed and now by the European Central Bank is actually depressing private-sector economic activity by taking money out of the hands of consumers and businesses.And by using bank reserves to acquire government and agency securities via QE, the Fed has been artificially pushing up the prices of financial assets around the world even as income and GDP stagnates. Public companies are using low interest rates to fund stock buy-backs instead of making new investments .. By robbing individual savers and financial institutions of income, and artificially boosting asset prices, the Fed and ECB are unwittingly creating the circumstances for the next financial crisis.” . Whalen advises ending financial repression.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/03/2015 - Rare Stamps & Coins – One Way to Beat Financial Repression

The Telegraph article & results from a new study on how investors can seek protection from the damaging impact of quantitative easing, low interest rates, low yields – financial repression – through rare stamps & coins .. “Stamps can’t be licked when it comes to an alternative investment .. Stamps and coins have become a viable alternative investment class that have outperformed the FTSE 100, according to new research.” .. Guy Tolhurst, managing director of Intelligent Partnership: “Stamps and coins present investors with one way to beat financial repression: the low interest rates, money printing and silent currency war that central banks are resorting to in order to stimulate the economy.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/02/2015 - FINANCIAL REPRESSION IS AN “OPAQUE TAX” ON YOUR PENSION & INSURANCE POLICIES

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

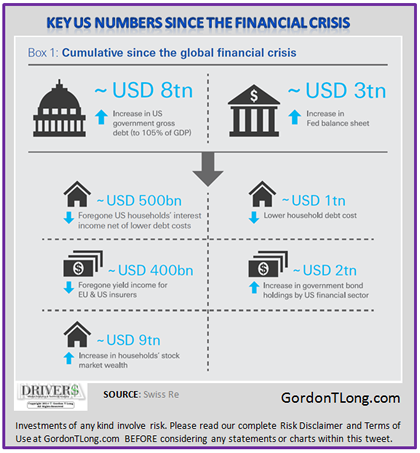

04/01/2015 - Swiss Re: Financial Repression has cost U.S. Savers $470 Billion

Swiss Re report highlights how artificially low interest rates have cost U.S. savers U.S.$470 Billion .. the report also explains how financial repression has exacerbated wealth/income inequality .. Swiss Re has also crafted a “Financial Repression Index” – see above .. “Looking ahead, financial repression is likely to remain a key tool for policymakers given the moderate global growth outlook and high public debt overhang. But, as outlined in this paper, financial repression comes with significant costs. Whether the costs outweigh the benefits largely depends on the ability of governments to take advantage of the low interest rate environment by implementing the right structural reforms. So far, their record for doing so has not been comforting, as also noted by the IMF .. Additional research on financial repression could be linked to the impact of an aging society on the broader economic and financial market environment and hence the optimal policy mix. Finally, a largely unexplored area is the consequence – especially longer-term – of public authorities acting as dominant players in their own bond markets. How does this affect private capital markets, and how severe are the distortions in price formation, investment decisions, allocation to productive areas and capital flows more generally?” .. the report includes a Foreward by Swiss Re Group Chief Investment Officer Guido Fürer.

FINANCIAL REPRESSION TAX TO SAVERS HAS BEEN ~$470B SINCE 2000

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/01/2015 - Financial Repression: Wealth Taxes on the Way

Charles Hugh Smith*: “As the global economy slides into recession and the U.S. economy catches a cold, the blueprint for raising taxes will be dusted off in every state .. Here’s the blueprint for raising taxes: 1. Declare the tax is an emergency measure. 2. Start the tax out at a low rate to minimize resistance. 3. Levy the tax only on the wealthy to play the “it’s only fair” card. 4. During some late-night session when the public isn’t looking, make the tax permanent by burying the provision deep inside some popular and/or complicated legislation. 5. Raise the tax rate in response to deficits, i.e. “we need more money.” 6. Gradually expand the base by reducing the qualification level from “wealthy” to “well-off” and eventually to everyone. 7. Gradually reduce deductions and exemptions to pittances. 8. Auction off exemptions for the super-wealthy via campaign contributions. You can watch the blueprint in action in any number of locales–for example, Rhode Island, where the governor is proposing a first-ever statewide property tax on second-homes worth more than $1 million. The proposed levy has been dubbed the Taylor Swift Tax in honor of Swift’s $17 million mansion on the Rhode Island coast.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/28/2015 - Financial Repression is causing Banknotes to become an Attractive Investment – This could cause a run on the Banking System

In his latest investment letter, Tim Price observes how the financial world is bifurcated into 2 camps – savers & speculators .. “All the forces of the world’s central banks have been devoted to shafting the former and encouraging the latter. The process ends badly. When Danish borrowers are paid to borrow by their banks and Danish savers are penalised for keeping money in the bank, something has gone gravely wrong with the financial system. Something is rotten, and not just in Denmark.” .. Price also references Russell Napier who thinks that physical cash – the banknote – is now becoming an increasingly attractive investment, but warns any significant move towards this “investment” will create a run on the banking system: “This has not happened. Yet. However, with the vast bulk of ECB purchases of assets still to come, the move to negative nominal interest rates has just begun. At some stage a shift to banknotes will begin and the limits to monetary policy will become much clearer. The spluttering torch of reflation will have to be passed to governments, and extreme government measures, such as outlawing cash holdings, are already under discussion. Investors should look to the imposition of a Tobin tax on capital inflows in Sweden, Switzerland or Denmark as a key indicator that central bank action will have to be bolstered by direct government intervention in markets.” .. we are in the era of financial repression.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/27/2015 - Financial Repression Is Creating Financial Bubbles

“This morning’s Wall Street Journal expressed it about as plaintively as it comes. In a word, the monetary politburo is waiting for zero interest rates, massive debt monetization and its wealth effects promises and “puts” to goose the macros: ‘The central bank has kept rates near zero since the recession to spur hiring, investment and spending.’ .. Does it really take purportedly intelligent people six years to see that the macros are not responding? Better still, isn’t it time for the Fed to explain the exact channel by which its interest rate pegging and forward guidance is supposed to be transmitted to the main street economy? After all, if these channels are blocked or ineffective then its flood of liquidity never leaves the canyons of Wall Street. In that event, the central bank actually functions as a financial doomsday machine, inflating the next financial bubble until it bursts. Then, apparently, its job is to rinse and repeat .. How in the world, it might be asked, is it possible that the chief beneficiary of the financial repression policies of the Fed is the very most affluent segment of society? That is a salient question—-but don’t bother to ask the liberal Keynesians who run the Fed. They do no even have a clue that it’s happening.” – David Stockman

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/26/2015 - Financial Repression Depresses The Economy

“ZIRP (zero interest rate policy) and QE (quantitative easing) as practiced by the Fed and ECB are not boosting, but instead depressing, private sector economic activity. By using bank reserves to acquire government and agency securities, the FOMC has actually been retarding private economic growth, even while pushing up the prices of financial assets around the world. ZIRP has reduced the cost of funds for the U.S. banking system from roughly half a trillion dollars annually to less than $50 billion in 2014.This decrease in the interest expense for banks comes directly out of the pockets of savers & financial institutions.While the Fed pays banks 25bp for their reserve deposits, the remaining spread earned on the Fed’smassive securities portfolio is transferred to the U.S. Treasury – a policy that does nothing to support credit creation or growth. The income taken from bond investors due to ZIRP and QE is far larger. No matter how low interest rates go and how much debt central banks buy, the fact of financial repressionwhere savers are penalized to advantage debtors has an overall deflationary impact on the global economy.Without a commensurate increase in national income, the elevated asset prices resulting from ZIRP and QE cannot be validated and sustained. Thus with the end of QE in the U.S. and the possibility of higher interest rates, global investors face the decline of valuations for both debt and equity securities.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/25/2015 - The “Natural Interest Rate” Is Always Positive And Cannot Be Negative! – Professor Dr. Thorsten Polleit

The True Purpose of Negative-Interest-Rate Policy

For some reason, those who argue that the originary interest rate has become negative seem to overlook that the originary interest rate is a phenomena which is not confined to credit markets. It pervades all markets in which present goods are exchanged for future goods.

For instance, the originary interest rate prevails at each stage of the economy’s time-consuming roundabout production. The originary interest rate also exists in the stock market, where investors exchange present money against a claim on future money (that is a firm’s dividend payment).

If they wanted to be consistent, the believers in a negative originary interest rate would have to call for a policy that does not only make interest rates negative in real terms in the credit market, but also in the markets for, say, stocks and housing.

However, a policy that advocates destroying firms’ values and peoples’ housing wealth wouldn’t be taken too kindly by the public at large; and those economists recommending it couldn’t expect being cheered.

The consequence of a policy of a negative real market interest rate should have become obvious by now:

It is an actually perfidious policy for debasing the real value of outstanding debt; and it is a recipe for wreaking havoc on the economy.

Market interest rates may become negative in real terms. In a “hampered market,” for instance, the central bank can push the real market interest rate into negative territory. However, this does not, and cannot, represent an equilibrium, as time preference and thus the originary interest rate cannot become negative.

Should a central bank really succeed in making all market interest rates negative in real terms, savings and investment would come to a shrieking halt: as time preference and the originary interest rate are always positive, “capitalistic saving” — the accumulation of goods designed for improving the production process — would come to an end. Capital consumption would ensue, throwing mankind back into poverty. It would be the end of the market economy.

It might be interesting to note in this context that, for instance, the German national socialists had called for the abolition, the prohibition of the interest rate. Now you know why: Without a positive (originary) interest rate, the market economy will cease to function.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/18/2015 - Financial Repression Explained: It’s about Macro Prudential Policies to Control and Reduce Government Debt

04/18/2015 - Financial Repression Explained: It’s about Macro Prudential Policies to Control and Reduce Government Debt